On 30 March 2023, the FCA held a webinar discussing their expectations for firms regarding the implementation of the Consumer Duty, which is set to take effect in just four months.

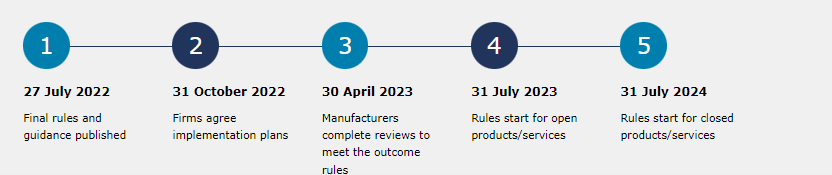

Reminder of key dates

Reminder of Consumer Duty application

The duty applies to retail customers. The FCA’s definition of retail customers goes beyond natural persons.

Payment service or e-money providers are subject to the Duty when dealing with consumers, micro-enterprises, and charities with a turnover of less than £1 million. Additionally, the Duty also applies to natural persons acting as trustees, but only if their actions fall outside their trade, business, or profession and in accordance with the “banking customer” test set out in the Banking Conduct of Business Sourcebook (BCOBS).

Neopay’s checklist on the outcomes

We’ve provided a summary of some of the key considerations to demonstrate how the four Consumer Duty outcomes have been considered and implemented. Your implementation plans should demonstrate how you assess compliance with the outcomes and what actions have been taken or planned to be taken.

Products and services

Products and services are designed to meet the needs, characteristics and objectives of a specified customer, based on a firms’ business models.

- Products and services are designed to meet the needs of consumers in the target market(s) and perform as expected.

- Identifying any features of the products and services which could cause harm to groups of customers with characteristics of vulnerability. What actions have been taken?

- Cross selling impact in scenarios where the promoted products or services were appropriate for the original target market, but not necessarily appropriate for all of a wider group of customers, creating a risk that the latter purchase products do not meet their needs.

- Information sharing with other firms in the distribution chain to ensure compliance with the Duty.

- Ongoing monitoring whether products and services continue to meet the needs of customers and contribute to good consumer outcomes. What data and management information is considered?

- Strong Customer Authentication (SCA) – effective and appropriate solutions that work for all groups of consumers, and consideration of the impact of SCA solutions on different groups of customers, in particular those with protected characteristics. Consideration of several different methods of authentication, such as methods that don’t rely on mobile phones, to cater to customers who don’t have/want to use a mobile phone, or need to make payments in areas without mobile phone reception.

PRICE AND VALUE

Products and services provide fair value with a reasonable relationship between the price consumers pay and the benefit they receive.

It’s more than just price, it is about a reasonable relationship between the price paid for a product or service and the overall benefit a consumer receives from it.

- Clarity of fees and charges, including regular and contingent fees and charges. For example, charging a redemption fee, requires the fee to be proportionate and commensurate with the costs actually incurred by the firm.

- Regular review of fees structure, in particular as costs to the business change.

- Adverse impact to the changes in fees and charges structure on vulnerable customers. For example, charging a minimum charge for topping up an e-money account may suggest customer who make frequent low value top-ups are paying more than customer with higher less frequent ones.

- Where products and services are distributed to retail customers through agents or distributors, firms must ensure fair value in relation to distributed products and services.

CONSUMER UNDERSTANDING

Firms communicate in a way that supports consumer understanding and equips consumers to make effective, timely and properly informed decisions.

- Clear information about fees and charges provided to customers at the right times, and presented in a way they can understand.

- Clarity on level of protection available on specific products. For example, clarity on how customer funds are protected through safeguarding, in absence of the Financial Services Compensation Scheme (FSCS), given that Payment institutions (PIs) or Electronic Money Institutions (EMIs) do not operate as banks.

- Clarity on which products are regulated, in scenarios where a firm provides range of regulated and unregulated services, to differentiate level of customer protections available.

- Where products and services are provided through agents or distributors, it must be made clear what are the responsibilities of the agent versus Principal.

- Avoiding use of technical or complex language that might be difficult for customers to understand. For example, when using open banking and asking for consent, it must be made clear what the consent is for to allow retail customers to make informed decisions.

CUSTOMER SUPPORT

Firms provide support that meets consumers’ needs throughout the life of the product or service.

The FCA does not prescribe which channels firms must offer, but expects that the channels are appropriate for customer types and their needs.

- Provide support throughout whole cycle, meaning that equal level of support should be available to customer prior and post account opening.

- Appropriate channels for customers. For example, online operating firms may not offer other channels for consumers to contact them if they are experiencing difficulties, such as being unable to access mobile and internet services, or if they need to speak to a member of staff directly to report fraud on their account.

- Make it clear and accessible for customers how to contact the firm or raise a complaint.

- Ease of moving to another product or exiting, if the product is no longer suitable for customers.

- Where account freezing is necessary due to identified financial crime activities and investigatory work taking place under the firms Suspicious Activity Report (SAR) regime. Whilst this is expected and reasonable in principle, firms must not freeze disproportionate number of accounts for too long, and without adequate explanation. Account freezing processes should be reviewed to make such scenarios less frequent (through more effective KYC/KYB processes and transaction monitoring), less protracted (through more efficient investigations), better communicated to customers (to the extent possible without tipping off) and better supported (considering putting customers into financial difficulties).

- Freezing of customers account (related to SAR) – when too many accounts are frozen or for too long – firms must not put any unreasonable barriers.

How we can help

For everything you need to know about the Duty and the requirements for your business, check out our dedicated FCA Consumer Duty section for the latest updates.

If you’d like to know more about how we can assist you with implementation of the Consumer Duty or how we can support you with authorisation arrangements, or any other regulatory compliance matters, please contact our specialist team here.