Fraud remains one of the biggest threats to the UK’s financial sector. The latest UK Finance Fraud Report for the first half of 2025 shows a concerning rise in criminal activity, with fraudsters becoming more organised, adaptable, and tech-savvy. As always, the data highlights the need for strong prevention strategies, industry collaboration, and ongoing investment in financial crime defenses.

At Neopay, we work closely with businesses to strengthen their compliance controls, enhance fraud prevention strategies, and ensure they remain resilient against evolving threats. This latest report further highlights why this work is essential.

Key highlights from the 2025 report

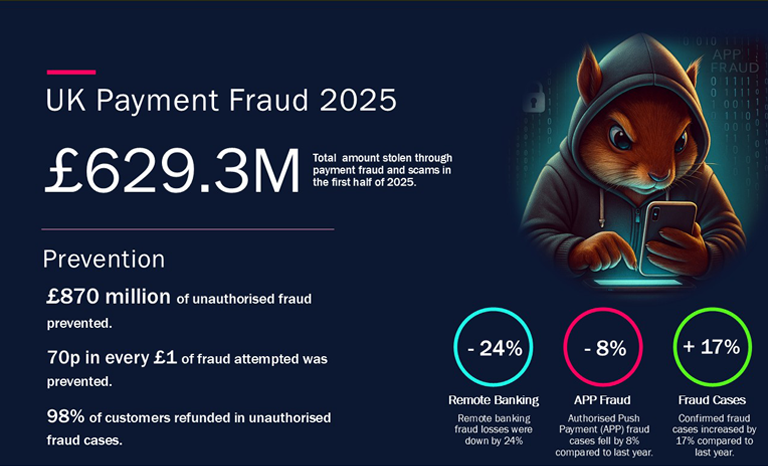

- Over £600 million stolen by criminals: £629.3 million was lost to fraud in the first half of 2025 — a 3% increase on the same period last year.

- Fraud cases surged by 17%: More than 2.09 million confirmed cases were reported, showing the scale and speed at which fraud tactics continue to evolve.

- £870 million in fraud prevented: Banks stopped 70p of every £1 attempted, a 20% improvement year-on-year thanks to advanced detection systems.

- Online and telecoms platforms continue to fuel fraud:

- 66% of Authorised Push Payment (APP) fraud cases began online.

- 17% originated through telecommunications.

- Industry calls for greater cross-sector accountability: While financial institutions continue to invest heavily in fraud prevention, UK Finance stresses that other sectors — particularly tech and telecoms — must take more responsibility.

UK Finance’s Managing Director of Economic Crime, Ben Donaldson, stressed the need for coordinated action, warning that fraud remains a significant threat to UK society and the economy, with criminals often manipulating victims long before a payment occurs.

Unauthorised fraud: losses down, cases up

Losses from unauthorised transactions — including card fraud, remote banking, and cheque fraud — totalled £372 million, representing a 3% decrease from H1 2024.

However, this came alongside a 19% increase in cases, reaching over 1.98 million incidents — a reminder that criminals continue to target large numbers of victims, often with smaller but more frequent attacks.

Notable trends:

- Cheque fraud losses fell by 41%, marking a significant decline.

- Remote banking fraud decreased by 24%, reflecting improved controls and customer authentication.

- Card-not-present fraud cases rose by 22%, driven largely by stolen card details being used online.

- Banks are still battling widespread social engineering, particularly where customers are tricked into handing over OTPs, enabling criminals to set up digital wallets and execute fraudulent transactions.

Positively, banks prevented £870 million of unauthorised fraud — a 20% increase — and more than 98% of victims are fully refunded under legal protections.

Authorised Push Payment (APP) Fraud: losses rise faster than cases fall

APP fraud remains one of the most damaging forms of financial crime, with £257.5 million lost — a 12% increase on last year.

Interestingly, APP case numbers fell by 8%, suggesting fraudsters are targeting fewer victims but achieving higher-value scams.

Key developments within APP fraud:

- Investment scams surged by 55%, stealing £97.7 million — often involving large sums and long-running deception.

- Purchase scams remain the most common, accounting for 72% of all APP cases, with losses up 10% despite a 7% fall in cases.

- Romance scam losses increased by 35%, showing the continued emotional and psychological manipulation used by fraudsters.

- Impersonation scams — involving criminals posing as police or bank staff — fell significantly, with cases down 16% and losses down 14%, helped by public awareness campaigns.

A total of £159.2 million was returned to victims in H1 2025, reflecting increased reimbursement under the Payment Systems Regulator’s enhanced rules introduced in October 2024. However, UK Finance notes that full comparability is challenging due to differences in scope.

APP fraud continues to be heavily driven by non-bank sectors:

- 66% of cases originated online — often via social media, fake adverts, or messaging platforms.

- 17% started via telecommunications networks, including phone calls and SMS spoofing.

UK Finance is urging the government to ensure that its upcoming Fraud Strategy holds these sectors accountable — both financially and operationally — for their role in enabling scams.

How Neopay can help

At Neopay, we understand the complexity of today’s fraud landscape. With fraud cases on the rise and criminals continuously evolving their tactics, it’s essential for businesses to stay ahead of the curve. Here’s how we can support you:

- Fraud prevention audits: Our audits help identify vulnerabilities in your business’s payment and security processes. By highlighting potential risks, we enable you to implement the necessary safeguards to protect against fraud.

- Compliance framework development: Ensuring your business meets all regulatory requirements is critical in avoiding penalties and reputational damage. We offer tailored compliance solutions that align with the latest industry regulations and fraud prevention strategies.

- Training and awareness programs: One of the most effective ways to prevent fraud is to ensure that your staff are aware of the latest threats. We provide engaging training programs that focus on practical, real-world scenarios, helping your team stay vigilant and equipped to identify suspicious activities.

- Ongoing support: Fraud is not a static threat. We provide continuous support, including regular updates on new fraud trends, changes in regulation, and best practices for maintaining robust security measures.

By working with Neopay, businesses can take a proactive approach to fraud prevention, ensuring that they are well-prepared to tackle the challenges of a rapidly changing fraud landscape. Contact our team to find out more about how we can protect both your business and your customers from the growing threat of fraud.