Open Banking, which allows third-party providers to access the financial information of banking customers through Application Programming Interfaces (APIs), was launched with the aim of providing customers with more tailored and innovative products and services, and to foster more competition in the banking industry.

As banks attempt to broaden and improve their digital offerings, countries and regions have approached Open Banking in different ways – states a new report “Open Banking: revolution or evolution?” written by the Economist Intelligence Unit (EIU) and based on a survey of over 300 global banking executives.

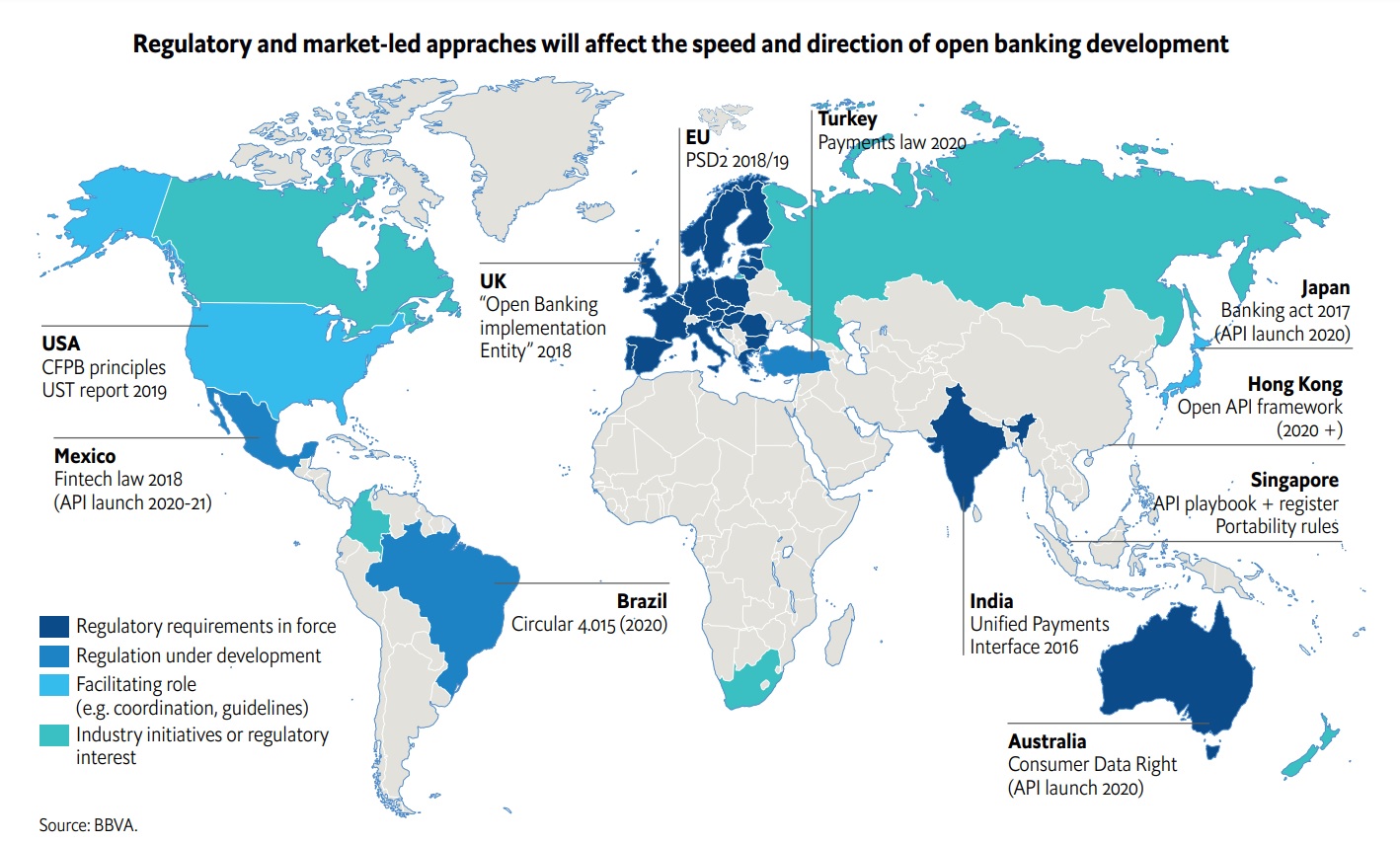

Some, like the US, take a market-led but fragmented approach. Asia has a mix of regulation, supervisory guidance and market-led approaches. Others, particularly the EU, have legislated, obliging all banks to open their data and payments—with customers’ consent—to third-party providers.

Globally, Open Banking could generate more innovation and competition, ultimately leading to a better end-user experience. Incumbent banks could be the biggest beneficiaries, providing that they adopt adequate technology strategies to compete with nimble new entrants.

While banking data is beginning to flow, according to the report, the global revolution in Open Banking is a work in progress and customer experience and confidence are key to unlocking its true potential.

The pandemic has boosted it and the financial technology ecosystem. The report states that incumbent banks could be the biggest beneficiaries, provided they adopt adequate technology strategies to compete with nimble new entrants.

The report finds Open Banking could benefit banks by making it easier for them to leverage their own data internally for better service personalisation, a top priority for nearly a third (32%) of respondents in the EIU survey.

Regulation has been the main driver in many regions, notably Europe and some Asian and Latin American countries.

In others, it has evolved owing to market forces and new competitors such as e-commerce giants in China and nimble challengers in the US.

The UK is leading the way in Open Banking due to regulatory requirements and a dedicated central program and platform, the Open Banking Implementation Entity, funded by the country’s nine biggest banks.

In Asia, large existing financial technology (fintech) platforms have developed open banking services in a low regulatory environment.

For instance, China’s Alipay and WeChat Pay exploited their huge social media and gaming platforms and customer bases to offer other services. Such firms needed to develop payment systems in a country where credit card penetration is low.

In effect, their closed ecosystems bypassed the banking system altogether, offering their clients AI-driven lending, wealth products and more. The fact that Asia-based users are broadly willing to share their data has reinforced this trend.

Australia, Mexico and Brazil have also introduced Open Banking legislation, while Canada has started the second phase of its “consumer-directed finance” consultation.

The report cautions, while 87% of countries reportedly have some form of open APIs in place, the evolution of Open Banking depends on customer confidence in sharing their data, interoperability, enhanced user experience, and actual added-value of products and services for customers.

“Open banking is lowering barriers to entry and breaking the traditional banking value chain. It is forcing banks to rethink their business models and decide whether they want to be manufacturers or distributors of financial products or both,” says Kanika Hope, Chief Strategy Officer, Temenos.

“Opening up banking isn’t enough unless you can prove to your customer base the certainty of how their data is going to be treated, certainty about refund periods and reconciliation information, or certainty about what happens if you do something wrong,” concludes John Broxis, Managing Director, Open Banking Europe.

Source: Payments Card and Mobile