FCA fines for FinCrime failings more than double in 2025

The value of FCA fines for Financial Crime failings has more than doubled in 2025 for the 2nd year in...

Read More

UKFIU Annual Report shows Denied DAML Requests up 59% [Infographic]

The UKFIU has published its SARs Annual Report which shows that Funds Denied from Defence Against Money Laundering (DAML) requests...

Read More

AML and Financial Crime training that delivers real business value, not just box-ticking

For many organisations, AML and financial crime training is something that simply must be done. It’s mandatory, often repetitive, and...

Read More

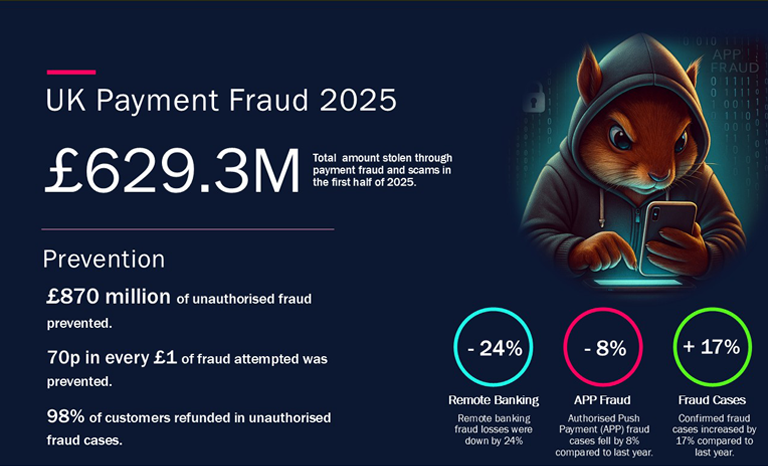

Key Insights from the UK Finance Half Year Fraud Report 2025

Fraud remains one of the biggest threats to the UK’s financial sector. The latest UK Finance Fraud Report for the...

Read More

Autumn Compliance Checklist: What Payment and E-Money Firms Need to Do Before Year-End

With year-end approaching, autumn is a natural time for payments and e-money firms to evaluate their compliance priorities, review frameworks,...

Read More

New UK Payments Infrastructure Strategy Outlines Key Outcomes for the Future of Retail Payments

The Payments Vision Delivery Committee (PVDC) — which includes HM Treasury, the Bank of England, the Financial Conduct Authority (FCA),...

Read More

FCA fines for FinCrime failings more than double in 2025

UKFIU Annual Report shows Denied DAML Requests up 59% [Infographic]

AML and Financial Crime training that delivers real business value, not just box-ticking

Key Insights from the UK Finance Half Year Fraud Report 2025

Autumn Compliance Checklist: What Payment and E-Money Firms Need to Do Before Year-End

New UK Payments Infrastructure Strategy Outlines Key Outcomes for the Future of Retail Payments

Chancellor launches new Scale-up Unit to accelerate growth for financial services firms

What the FCA’s latest strategy means for payments and e-money firms

Draft Money Laundering Regulations Published for Technical Consultation